Pune registers warehousing transactions of 7.4 mn sq ft in FY 2023

Mumbai, 13th June 2023: Knight Frank India, an International Property Consultant, in their latest report, ‘India Warehousing Market Report 2023’, cited that Pune recorded warehousing transactions of 7.4 mn sq ft in FY23 and ranked 4th amongst the top 8 cities. On YoY basis, the city reported a marginal decline of 2% from 7.5 mn sq ft in FY22.

Warehousing transactions across top 8 Indian cities

| Warehouse leasing | FY23 | % Change | CAGR |

| City | mn sq ft | FY23 YoY | FY17-23 |

| Mumbai | 9.5 | 10% | 35% |

| NCR | 8.6 | -5% | 20% |

| Bangalore | 7.4 | 25% | 34% |

| Pune | 7.4 | -2% | 24% |

| Kolkata | 5.1 | 18% | 25% |

| Hyderabad | 5.1 | -7% | 27% |

| Chennai | 4.5 | -11% | 16% |

| Ahmedabad | 3.8 | -29% | 14% |

| Total | 51.3 | 0% | 24% |

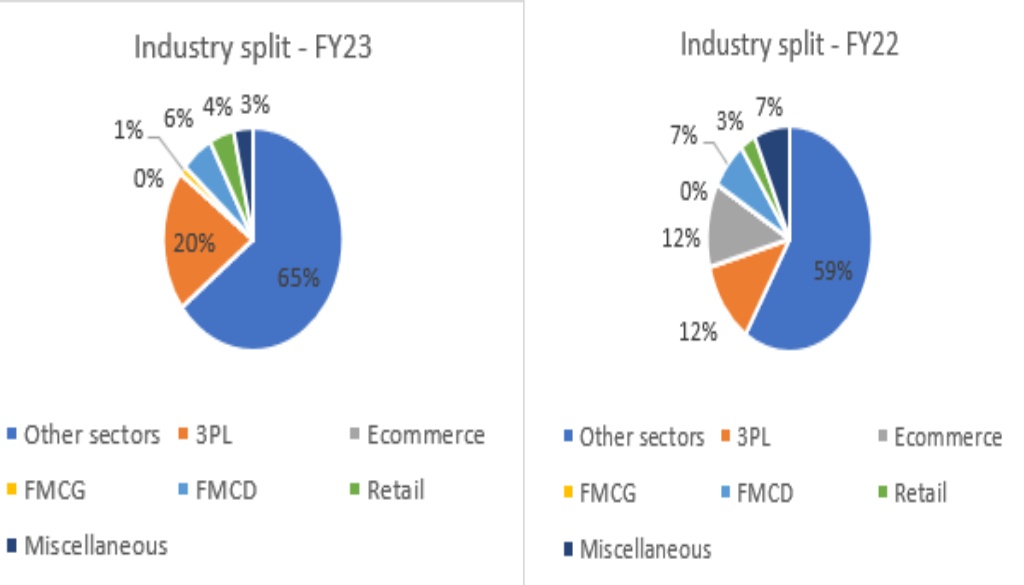

As far as the industry-split of transaction volume is concerned the ‘Other sectors’ which includes manufacturing sectors (automobile, pharmaceutical, etc.) excluding FMCG and FMCD has emerged as the largest driver for the warehousing demand in FY23. The demand was primarily seen from the major automakers such as Hyundai and Tata as Pune’s profile as an important manufacturing destination continues to grow. The sector accounted for 65% of the region’s warehousing transactions, compared to 59% in FY22. In FY23, 3PL sector witnessed an 8% increase in share of transaction volumes from 12% in FY 22 to 12% in FY23.

Industry-split of transaction volume

Cluster Split

With respected to cluster split transactions, Chakan–Talegaon warehousing belt garnered 83% share of the total transactions during FY23. The Chakan MIDC has matured into a manufacturing and industrial centre and is referred to as the ‘Automobile hub’ in Maharashtra due to its significant automobile industry presence.

The manufacturing and 3PL occupiers recorded space take up in FY23 in the Chakan–Talegaon belt despite their high rentals, as the belt offers good quality high-quality Grade-A spaces within a developed cluster with the necessary ancillary services. Other accounted to 15% of the total transaction while Wagholi–Ranjangaon belt accounted for 2% of the total transaction volume during the period.

Shishir Baijal, Chairman and Managing Director, Knight Frank India said, “The warehousing market has experienced consistent growth, with transaction volumes exceeding the previous year’s figures, which were already the highest in history. This growth is not limited to the top eight markets but has also extended to secondary markets, supported by enhanced infrastructure such as highway networks, rail systems, and air transportation. Indeed, there has been a noticeable shift in the occupier groups within the warehousing market. Third-party logistics (3PL) providers and manufacturing companies have emerged as the primary players, indicating their increasing importance in the industry. As these occupiers take the lead, their evolving needs and preferences regarding warehousing requirements have become significant factors to consider. Occupiers have specific demands and expectations when it comes to warehousing facilities. They seek spaces that can accommodate their storage and distribution operations efficiently. Flexibility, scalability, and customization options are crucial for meeting their evolving needs.”

Pune: Land Rate and Rents

Pune market has recorded warehousing rental escalation of 4.4% YoY with an average rent of INR 258/sq m/month (Rs 24/sq ft/month) in FY23. Locations like Talegoan and Ranjangaon recorded upward rent movement in the Grade-A spaces while owing to its high demand Chakan is the only market that recorded rent escalations in both Grade-A & Grade-B spaces.

Grade-A rentals in the Chakan-Talegoan belt range from INR 215-334/sq m/month (INR 20-31/sq ft/month) while rentals in the Wagholi-Ranjangaon belt range from INR 172-269/sq m/month (INR 16-25/sq ft/month).

| Warehouse cluster | Location | Land rate (INR mn/acre) | Rent in INR/sq m/month (INR/sq ft/month) | |

| Grade A | Grade B | |||

| Chakan-Talegaon belt | Chakan | 22-28 | 301-334 (28-31) | 226-269 (21-25) |

| Talegaon | 20-25 | 215-258 (20-24) | 172-194 (16-18) | |

| Kuruli | Large land parcels not available | No Grade A supply | 151-172 (14-16) | |

| Chimbali | Large land parcels not available | No Grade A supply | 151-172 (14-16) | |

| Wagholi-Ranjangaon belt | Wagholi | Large land parcels not available | 215-269(20-25)

|

161-183 (15-17) |

| Lonikand | 15-20 | 172-183 (16-17) | 140-161 (13-15) | |

| Chakan-Shikrapur Road | 12-16 | 194-215 (18-20) | 151-172 (14-16) | |

| Sanaswadi | 14-18 | No Grade A supply | 140-161 (13-15) | |

| Ranjangaon MIDC | 18-20 | 194-237 (18-22) | 151-183 (14-17) | |

| Others | Shirwal | 13-16 | 172-194 (16-18) | 151-161 (14-15) |